A landed property is one where the erected house is on land that is also owned by the house owner.

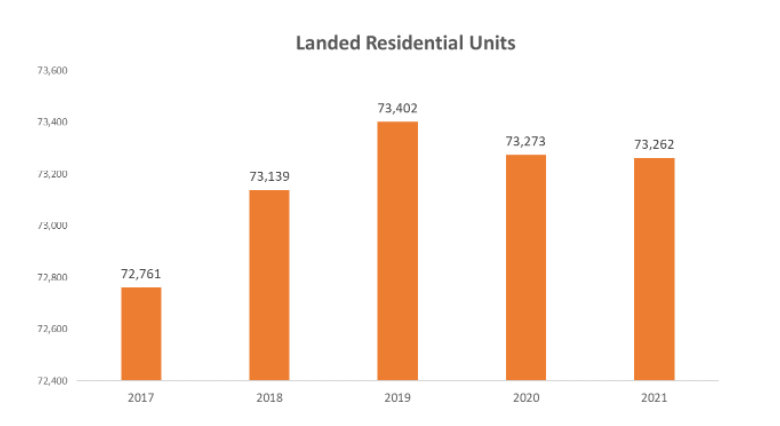

As of 2021, there are about 73,000 landed property units in Singapore. It’s rare to see new launches of landed properties, as they are in limited quantities.

Interest for landed property transactions have grown over the years as demand for such properties have increased since 2019 for both new and resale transactions. The number of landed transactions have also risen from over 2,000 units being transacted in 2020 to over 3,000 units being sold in 2021.

If you are new to landed properties, here are a few things to know about who can actually purchase landed property.

1. Singapore citizens and select foreign persons

According to the Singapore Land Authority (SLA), a foreign person is any person who is not a:

- Singapore citizen;

- Singapore company;

- Singapore limited liability partnership; or

- Singapore society

The SLA has FAQs here on the Clearance Certificate needed by firms and societies for their purchase of landed residential property.

If a foreign person wishes to purchase a landed residential property, he or she is required to seek approval under the Residential Property Act. All applications have to be submitted online here.

Each applicant will be assessed on a case-by-case basis, taking into consideration, but not limited to, the following factors:

- Should be a Singapore permanent resident for at least five years; and

- Must have made exceptional economic contributions to Singapore. This is assessed taking into consideration factors such as employment income assessable for tax in Singapore.

Some types of properties for which a foreign person must seek approval to purchase:

Terrace house

A terrace house is a dwelling house with its own land title that forms part of a row of at least 3 dwelling houses abutting the common boundary party walls.

Semi-detached house

A semi-detached house is one half of a pair of two houses, each with its own land title, separated by a common party wall along one side of the premises.

Bungalow/detached house

A bungalow is a detached landed house with its own land title.

Others

Strata landed house which is not within an approved condominium development under the Planning Act (e.g., townhouse or cluster house);

Shophouse (for non-commercial use).

2. Those with TDSR of 55% and below

In Singapore, property buyers must have a Total Debt Servicing Ratio (TDSR) of less than or equal to 55% (effective 16 Dec 2021).

The maximum threshold of this debt-to-income ratio is set by the Monetary Authority of Singapore and applies to not only individuals but also certain companies. The ratio must be calculated for any loan to purchase a property, any loan secured by a property, as well as the refinancing of these loans.

Financial institutions may still grant property loans to borrowers whose TDSR exceeds the threshold on an exceptional basis, subject to enhanced credit evaluation.

While the TDSR is a MAS rule, buyers of landed properties must also be aware that bank’s have their own loan limits.

What affects loan amount and tenure?

The maximum housing loan borrowers can take usually depends on their age, loan duration and property type, and whether they have existing housing loans. Joint borrowers are assessed using an income-weighted average age.

In Singapore, the maximum home loan tenure for non-Housing Development Board properties is capped at 35 years.

How much can one borrow?

Currently, the loan-to-value (LTV) limit is 75%; or 55% if the loan tenure is more than 30 years or extends past age 65. LTV refers to the loan amount as a percentage of the property’s value and its limit determines the maximum amount an individual can borrow from a financial institution for a housing loan.

Other factors that can lower LTV include:

- Remaining lease on the property

- Location and state of the property

- Your credit score

And so, if you are a Singaporean, a Singapore firm with the required clearance certificate or a foreign person with the government’s approval to purchase, a landed property could be in your future if you so desire, provided your total debt servicing ratio is 60% or below. These are the first hurdles to overcome at least.

Looking for a landed property?

Let Ohmyhome’s smart data-matching technology MATCH you with the right home, according to your specific needs. Submit your preferences to us and our algorithm will filter all our available listings based on those, and we’ll WhatsApp them to you once we find a match. We’ll also send you relevant content that you can use for your research and inform your home buying decision, so you no longer have to spend hours searching online for the information that you need.

You can also secure an appointment with any of our Super Agents by dropping us a message on WhatsApp or chatting with us via our Live Chat at the bottom, right-hand corner of the screen.