As the year draws to a close, we’re looking back at the property moments that have impacted homeowners the most. There’s the 15-month wait-out period haunting Private Property Owners, which prevents them from selling their home for a HDB flat immediately after. We talk more about that here.

But that’s not the only cooling measure plaguing homeowners. There’s also the matter of rising interest rates that practically everyone who currently owns a home or is planning on buying a home has to contend with today.

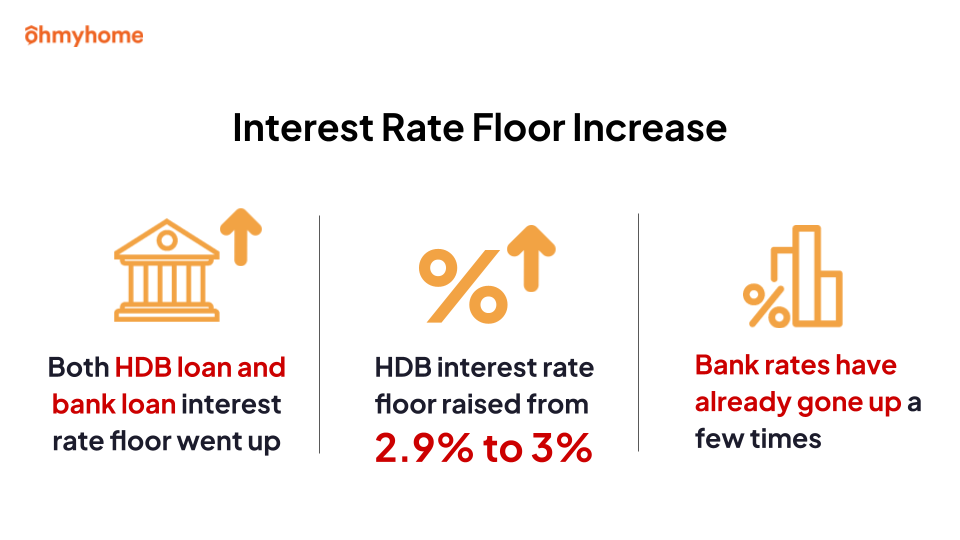

HDB interest rate floor rise to 3%

While the interest rate for a HDB loan is still 2.6%, which is the amount you are charged for borrowing and which is always pegged 0.1% above the CPF OA rate (it’s currently 2.5%), the interest rate floor has gone up from 2.9% to 3%.

To clarify, the interest rate floor is the factor that you use to calculate how much you can borrow for your loan. It basically acts as a ‘stress test’ that ensures you, the borrower, will be able to comfortably afford your home purchase and service your loan — in case the interest rate does rise to 3%, for example.

Possibility of CPF OA rate also increasing

Now, one of the reasons this matter is because the HDB interest rate is pegged to the CPF OA rate, and the rise of the interest rate floor gives way to the possibility that the CPF OA will also increase.

Bank rates have already gone up a few times this year, with the current interest rate now up to 4.5% for financial institutions such as DBS, OCBC, and UOB.

Another reason why the interest rate increase is important is that it directly impacts the affordability of your home because you’ll be forced to borrow less.

The reason why this matters is that when the interest rate floor increases, the amount you can borrow from either HDB or the bank will then decrease as a result.

The impact of rising interest rates (in numbers)

For example, let’s say you take a $1 million loan for 25 years. Before the cooling measures, with the bank rates at around 1.2%, you would only have to pay at least $3.9k per month. Now that the interest rates have risen to over 4%, you will have to pay about $5.4k a month, which is at least $1.5k more. That’s a 40% increase for the same housing loan.

This is pretty much the reality that homeowners are facing right now and the reason why many are dealing with ‘mortgage stress’.

A survey conducted by OCBC shows that about 40% face difficulties in paying off their mortgage loans, up from the 31% who dealt with the same stress in 2021.

On top of the rising interest rates, there’s also the lower Loan-to-Value limit, which dropped from 85% to 80%. Though this only affects those who have or will be taking a HDB loan, you will still have to borrow less — and that 5% will have to now be paid out-of-pocket.

During our Consumer Seminar on 29 November, UOB’s Mortgage Specialist Desmond Chua shared 3 ways you can potentially increase your mortgage loan:

- Increase your income

- Reduce your debt obligations

- Max out your loan period

3 ways to increase the amount you can borrow for your housing loan:

#1: Include your Eligible Financial Asset (EFA) value to your gross monthly income

You’re allowed to include your Eligible Financial Assets, such as cash, structured deposits, shares, stocks, trust, etc., to be recognised as part of your gross monthly income.

With a higher gross monthly income, you can qualify for a higher loan.

#2: Pay off other existing debts

On the other hand, you can pay off your other existing loans, such as car loans, student loans, and credit card loans, in order to raise your loan eligibility. Offloading your other debt obligations can mean a significant increase in the maximum loan amount you can borrow.

#3: Max out your loan tenure

While this may mean that you’re paying off your home loans for a longer period of time, you will actually pay less per month, which means you can actually borrow more for your home loan.

If you’re taking a HDB loan, the maximum loan tenure is 25 years or up to 55 years old, whichever is shorter. For a bank loan, the maximum loan tenure is 30 years if you’re buying a HDB flat and 35 years if you’re getting a private property.

Feeling the mortgage stress too?

Discover the best home loan rates across all the banks, and let us draw the comparisons for you. We’ll find you the best loan tailored to your needs – free of charge. Because at Ohmyhome, we’re always by your side, always on your side.

You can connect with our bank partners by simply filling out the booking form below, dropping us a message on WhatsApp or on the Live Chat at the bottom, right-hand corner of the screen.

We talk about another cooling measure released in 2022 — the 15-month wait-out period — that you can read right here.